{kind=link}

What is it?

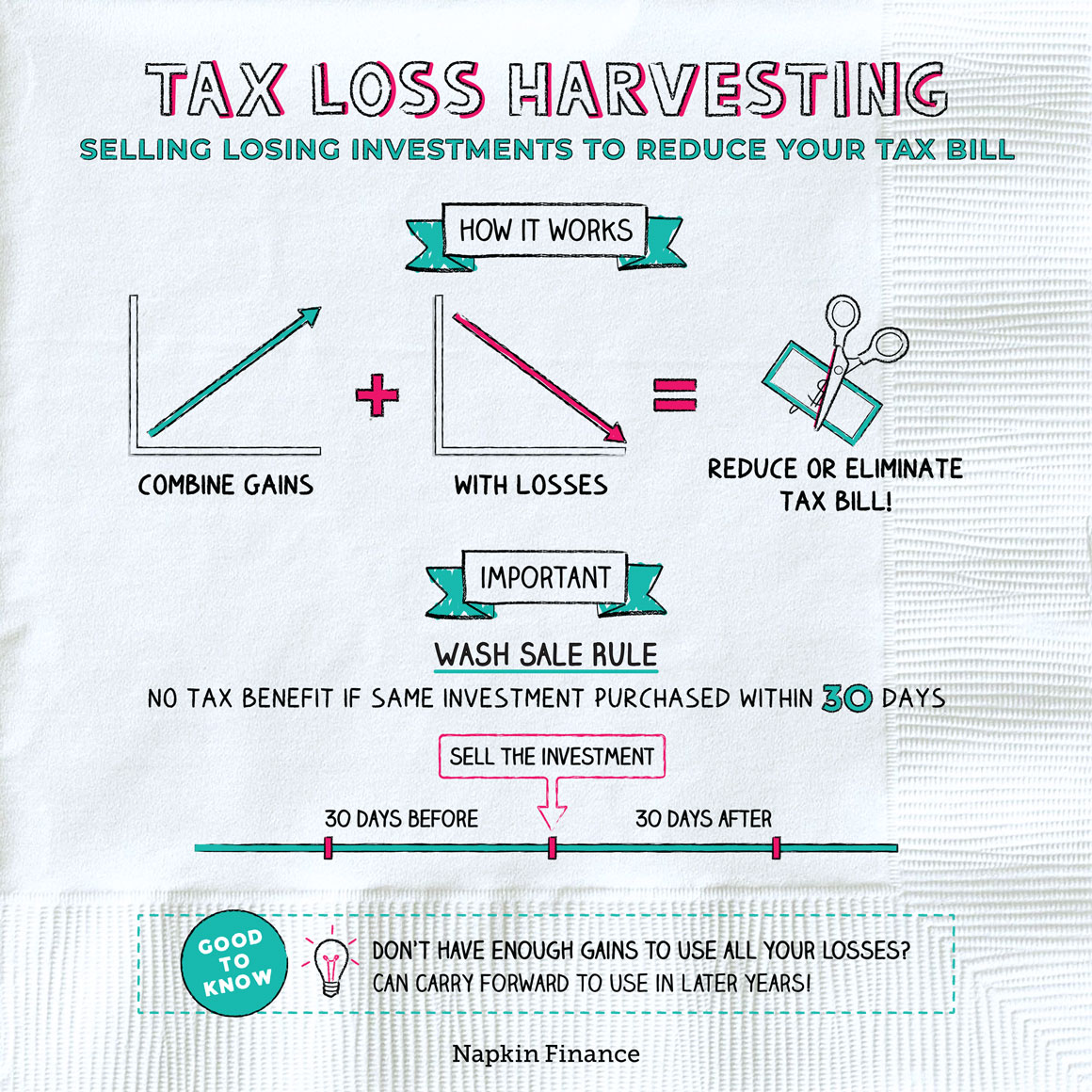

Tax-loss harvesting, in simple terms, involves the selling of securities when investments sustain a capital loss. The losses offset the values in tax returns from the income for that year. Likewise, investment gains can be offset by the sold asset. Tax-loss harvesting generally takes place during the end of the fiscal year. However, investors may harvest it at any time during the tax year. In this article, we explore how tax-loss harvesting works in the United States as well as the buyback rule.

Tax-loss harvesting is important in reducing the blow investors may face during capital loss. However, it becomes necessary to keep a look out for potential wash sales and buybacks. These occur when investors sell stocks at a loss to offset the tax from capital gains. A buyback occurs after a wash sale wherein the investor knowingly purchases or ‘buys back’ substantially identical stock.

How does it work in the US?

In the United States, this occurs entirely per definition where investors are able to offset their capital gains with any losses they had sustained during that tax year. This in turn allows them to reduce their tax bills, especially when facing a greater capital loss.

The buyback rule in the US iterates that a wash sale occurs when a stock sold at a loss is bought back within 30 days of the investment being sold. Investors need to adhere to a minimum of 31 or more days before purchasing any similar securities.

The buyback rule and how it works

Unlike in countries such as Australia, the US have distinct laws regarding the buyback rule.

In the United States, tax-loss harvesting occurs entirely per definition where investors are able to offset their capital gains with any losses, they had sustained during that tax year. This in turn allows them to reduce their tax bills, especially when facing a greater capital loss.

The IRS (Internal Revenue Service) Wash Sale Rule (IRC Section 1091) in the United States prohibits investors from selling a stock or security at a loss and within 30 days of this, repurchasing a substantially identical stock or security. This rule prevents investors from attempting to offset their tax bills during taxation time only to buy back the stock thus maintaining their income. The wash sale rule also applies to a person who attempts to sell a security, wherein the spouse or company of the person purchases an equivalent stock.

For example, if John owns Stock X with a value of $30,000. This stock has suffered a loss and the value has decreased to $20,000. Therefore, John sells Stock X on November 5th, to realize a capital loss of $10,000 for tax-loss purposes. However, on November 26th John repurchases the same Stock X. This would be counted as a wash sale and refuted from a tax reduction.