{kind=link}

30% of Australians were born overseas. It’s common for family funds to be moved to/from Australia to other family members/accounts. If you are receiving funds, however, many often forget that being a taxpayer in Australia means gifts received are subject to tax! Even if you/your family has already paid taxes on those funds in a different country. In this article, we will explore the daunting Section 99B and its effects on taxpayers in Australia.

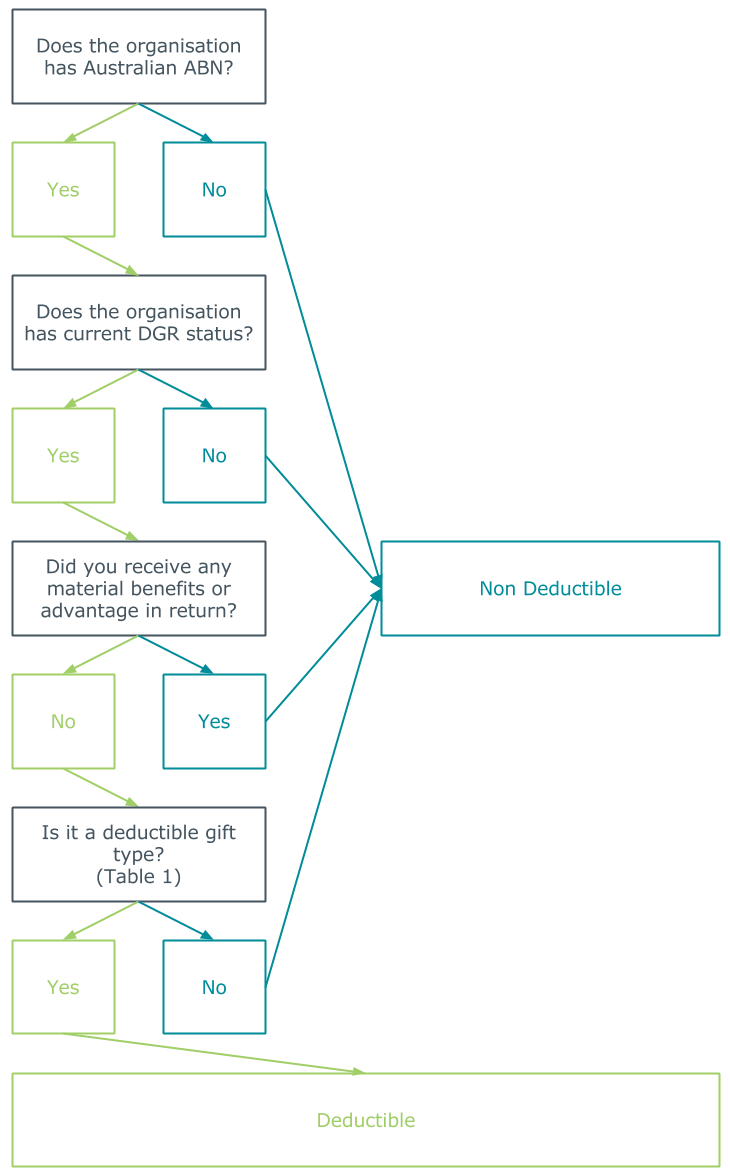

The ATO and Gifts

According to the ATO, tax reductions for gifts apply if the organization or person being gifted classifies as a deductible gift expense. If it is a DGR, the donor can claim for a reduction.

When receiving gifts from family abroad, they must fulfill the following requirements to be considered a genuine gift:

- the transaction of the gift possesses proper documentation

- both parties have behaviour supporting the giving and receiving of a gift

- the money received comes from trusts independent of the receiver

Section 99B

Section 99B in the Income Tax Assessment Act 1936 applies to any asset given out of a trust to an inheritor that is a tax resident. (You can find out more on this here). There are, however, a number of exemptions which include:

- Anything paid from the capital of the trust

- Amounts previously assessed to inheritor

- Amounts if converted by inheritor would not count as assessable income

For you to avoid assessment by the ATO, you would need proof that your payment came from the capital of a trust.

Migrants and s.99B – In Australia’s large migrant population, many family members abroad send money to their families in Australia. When these trusts pay money to an Australian taxpayer, s.99b often applies.

For example, Zhang is a tax resident in Australia. His father sent him a sum of $150,000 from China. If Zhang cannot prove the amount came from a capital of a trust, he will be subject to s.99B.

Conclusion

You should educate yourself about Section 99B in the event that you or your donor do not possess enough documentation for the gift received. It is important to also be aware of the implications of lacking proof under the ATO and S.99B. While Australians are lucky when it comes to estate taxes, this area is treated a bit differently.

Basically, always make sure to have supporting documentation that shows the money comes from the capital of a trust!